From Private to Public: How Does a Company 'Go Public' with an IPO?

Every share of stock you have ever bought was, at some point, created. Not printed — created, through a legal and financial process that transforms a privately held company into one that anyone with a brokerage account can own a piece of. That process is called an Initial Public Offering, and it is far more complicated, expensive, and strategically loaded than the opening-bell photo opportunities suggest.

What Is an IPO? The Plain-Language Definition

Private vs. Public Ownership

A private company is owned by a relatively small group — founders, early employees, and investors like venture capital firms. These owners cannot easily sell their stakes because there is no open market for the shares. An IPO changes that by creating new shares (or making existing ones available) and listing them on a public stock exchange, where anyone can buy and sell them freely.

The "initial" in IPO simply means it is the first time the company's shares are offered to the general public. After that, any subsequent share sales are called secondary offerings. The IPO is the door opening — everything after is just traffic through it.

Why Companies Do It

The most obvious reason is to raise capital. A company that goes public can bring in hundreds of millions — sometimes billions — of dollars in a single day, which it can use to fund expansion, pay down debt, or invest in research. But there is a second, less-discussed reason: liquidity for early investors and employees. Venture capital funds have a lifespan. They need to return money to their own investors eventually, and an IPO gives them a clean exit.

There is also a prestige dimension. Being publicly listed signals a certain level of institutional legitimacy — audited financials, regulatory oversight, a market-determined valuation. For some companies, that credibility matters as much as the cash.

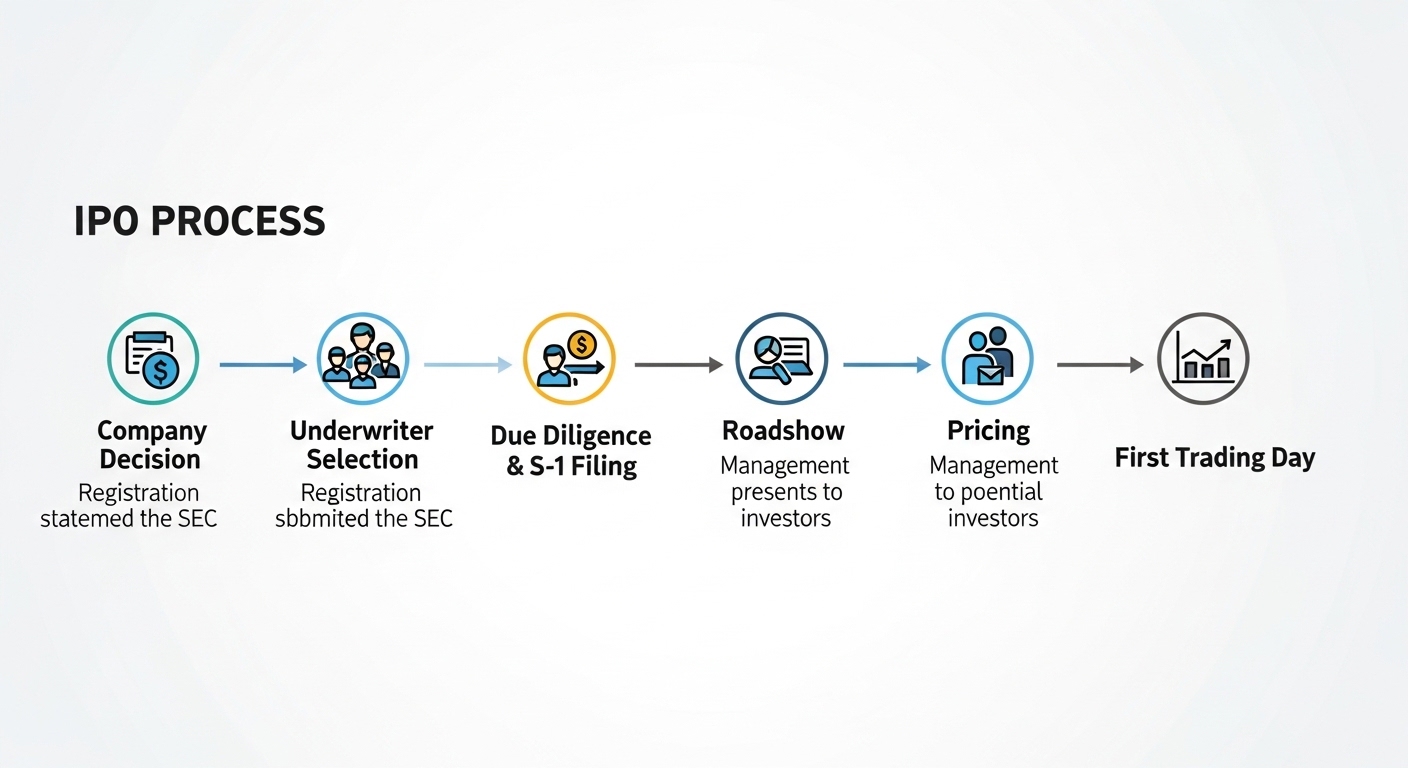

How the IPO Process Actually Works — Step by Step

Choosing Underwriters

The company hires one or more investment banks to manage the offering. These banks are called underwriters, and their job is substantial: they help set the initial share price, buy the shares from the company, and then resell them to institutional investors. The lead underwriter is often called the bookrunner. Major banks compete aggressively for this role because the fees — typically a percentage of the total money raised — can be enormous.

The underwriter relationship is not just transactional. Banks bring their existing network of institutional clients who will buy large blocks of shares. Without that distribution network, a company would struggle to place millions of shares in a single day.

Filing the S-1 and the Quiet Period

Before a company can sell shares to the public in the United States, it must file a registration statement — commonly called an S-1 — with the Securities and Exchange Commission. This document is dense and deliberately exhaustive. It includes audited financial statements, a description of the business, identified risk factors, and details about how the proceeds will be used. Reading an S-1 is one of the most direct ways to understand a business, because the company is legally required to disclose things it would rather not.

Once the S-1 is filed, the company enters a "quiet period" during which it is restricted in what it can say publicly about the offering. This rule exists to prevent companies from hyping their own stock before it is listed. Anyone who has watched a CEO suddenly go silent on social media right before a major announcement has probably seen this in action.

The S-1 filing is the most honest document a company will ever publish — because lawyers, not marketers, are in charge of what goes in it.

The Roadshow

With the S-1 under review, company executives and bankers embark on what is called a roadshow — a series of presentations to large institutional investors like mutual funds, pension funds, and hedge funds. The goal is to generate demand and gauge what price the market will actually support. Historically, this meant weeks of in-person meetings across major financial cities. More recently, virtual roadshows have become common, compressing the timeline considerably.

Investors who attend the roadshow can indicate how many shares they want and at what price. The underwriters aggregate this demand in a process called bookbuilding, which informs the final IPO price set the night before trading begins.

Pricing and the First Day of Trading

The IPO price is set after the market closes on the day before listing. This is where things get genuinely interesting. If the price is set too high, the stock may fall on its first day — a bad look that can damage confidence. If it is set too low, the stock "pops" dramatically on opening day, which looks exciting but actually means the company left money on the table. A 40% first-day pop sounds like a success story; from the company's perspective, it means they sold shares for far less than the market was willing to pay.

Who Gets Shares Before the Public Does?

The Allocation Problem

Here is the part most retail investors do not realize: by the time a stock opens for trading on its first day, the IPO shares have already been allocated — almost entirely to institutional investors. The large mutual funds and hedge funds that attended the roadshow receive shares at the IPO price. Retail investors buying on the open market are typically paying whatever the stock jumps to after those institutions receive their allocation.

This is not a conspiracy; it reflects the practical reality that institutions can commit to buying millions of shares reliably, while retail demand is unpredictable. But it does mean that the celebrated "IPO price" is largely a price that ordinary investors never actually get.

Lock-Up Periods

Insiders — founders, early employees, and pre-IPO investors — are typically subject to a lock-up period, usually around 180 days, during which they cannot sell their shares. This prevents a flood of insider selling immediately after the IPO, which would crater the price. When the lock-up expires, it is common to see a stock dip as insiders finally take profits. Savvy investors watch lock-up expiration dates the way they watch earnings reports.

What the IPO Costs — and What Companies Give Up

The Financial Toll

Going public is expensive in ways that surprise people. Underwriting fees alone typically run somewhere between 5% and 7% of the total capital raised for a standard offering. Add legal fees, accounting costs, SEC filing fees, and the expense of building out investor relations infrastructure, and the bill can reach tens of millions of dollars before a single share is sold.

Then there are the ongoing costs. Public companies must file quarterly and annual reports, hold earnings calls, comply with Sarbanes-Oxley requirements, and maintain a dedicated team to handle investor communications. For smaller companies, this overhead can be genuinely burdensome.

The Loss of Control

The subtler cost is autonomy. Once a company is public, its executives answer to shareholders and, by extension, to quarterly earnings expectations. A founder who wants to make a bold, long-term bet that will hurt short-term profits now has to justify that decision to thousands of investors — some of whom will sell the stock in protest. This pressure is real and well-documented. Several high-profile founders have taken their companies private again specifically to escape it.

Going public does not just change who owns the company — it changes how decisions get made, and on what timeline.(Opinion: The quarterly earnings cycle is probably the single most distorting force in public company strategy. The pressure to hit a number every 90 days pushes executives toward decisions that look good on a short timeline and terrible on a long one. It is a structural flaw that the market has largely decided to live with.)

Alternatives to a Traditional IPO

Direct Listings

A direct listing skips the underwriters entirely. The company does not issue new shares or raise new capital — it simply lists existing shares on an exchange and lets the market find a price. This saves on fees and avoids the dilution of new share issuance, but it also means no guaranteed capital raise and no institutional anchor buyers. A handful of well-known technology companies have used this route successfully, though it remains less common than a traditional IPO.

SPACs

A Special Purpose Acquisition Company — a SPAC — is a shell company that raises money through its own IPO with the sole purpose of merging with a private company later. For the target company, merging with a SPAC is a faster, more predictable path to public markets than a traditional IPO. SPACs had a dramatic surge in popularity in the early 2020s, followed by an equally dramatic pullback as many SPAC-merged companies underperformed. The mechanism is legitimate; the execution record has been mixed.

Why the Traditional IPO Survives

Despite the alternatives, the traditional underwritten IPO remains the dominant path for large companies going public. The underwriter's distribution network, price-setting expertise, and institutional relationships are genuinely hard to replicate. For a company raising several billion dollars, having a major bank stake its reputation on the offering still matters.

Frequently Asked Questions

Can individual investors buy shares at the IPO price?

Rarely, and only through specific channels. Some brokerage platforms have arrangements that allow retail clients to participate in IPO allocations, but the available shares are typically a small fraction of the total offering. Most individual investors end up buying on the open market after the stock begins trading, which is usually at a higher price than the IPO price.

Does a company have to be profitable to go public?

No. Many companies go public while still operating at a loss, particularly in technology and biotech sectors. What matters to underwriters and investors is the growth trajectory and the credible path to profitability. That said, unprofitable companies face more scrutiny in the S-1 process and tend to see more volatility after listing.

What happens to the original investors after an IPO?

Early investors — venture capital firms, angel investors, and early employees — typically hold shares that become publicly tradeable after the lock-up period expires. Many will sell at least a portion of their holdings at that point, which is the liquidity event they have been working toward. Some long-term investors hold their positions for years after the IPO if they believe the company still has significant growth ahead.

The IPO process is, at its core, a negotiation between a company's ambitions and the market's appetite — conducted in public, under regulatory scrutiny, with billions of dollars and years of work riding on a price set the night before trading begins. What looks like a celebration on opening day is actually the end of a months-long gauntlet. The bell ringing on the exchange floor is not the start of something; it is the conclusion of it. Everything that comes after — the quarterly reports, the analyst calls, the shareholder letters — is the actual job of being public, and it never really ends.

Comments

Post a Comment