Beyond the Piggy Bank: Creative and Unusual Ways to Save Money

A standard savings account earning a fraction of a percent while inflation quietly erodes your balance is not a strategy — it's a waiting room. The most effective savers tend to use a mix of psychological tricks, structural changes, and genuinely counterintuitive habits that most personal finance articles skip right past. Some of these approaches feel almost too simple. Others require a one-time setup that pays off for years. All of them work better than staring at a budget spreadsheet and feeling guilty.

#1–#3: Rewire How You Think About Spending

#1 — The 'Cost Per Use' Mental Reframe

Instead of asking 'how much does this cost?', ask 'how much does each use cost?' A $200 jacket you wear 150 times costs less per use than a $40 jacket you wear four times before it falls apart. This reframe naturally steers you toward fewer, better purchases — which is almost always cheaper over a three-to-five year horizon.

The same logic works in reverse as a spending brake. Before buying something impulsive, estimate how many times you'll realistically use it. Most people find the number embarrassingly low, and that alone kills the purchase.

#2 — The 24-Hour Rule (With a Twist)

The classic 24-hour waiting rule for non-essential purchases is well-known, but the twist that makes it work better is writing down exactly why you want the item right now. When you revisit the note a day later, the emotional urgency has usually evaporated. You're reading a message from a slightly different version of yourself, and that distance is surprisingly effective.

Research on impulse buying consistently suggests that the desire to purchase peaks quickly and fades within hours. The note makes that gap visible in a way that simply 'waiting' does not.

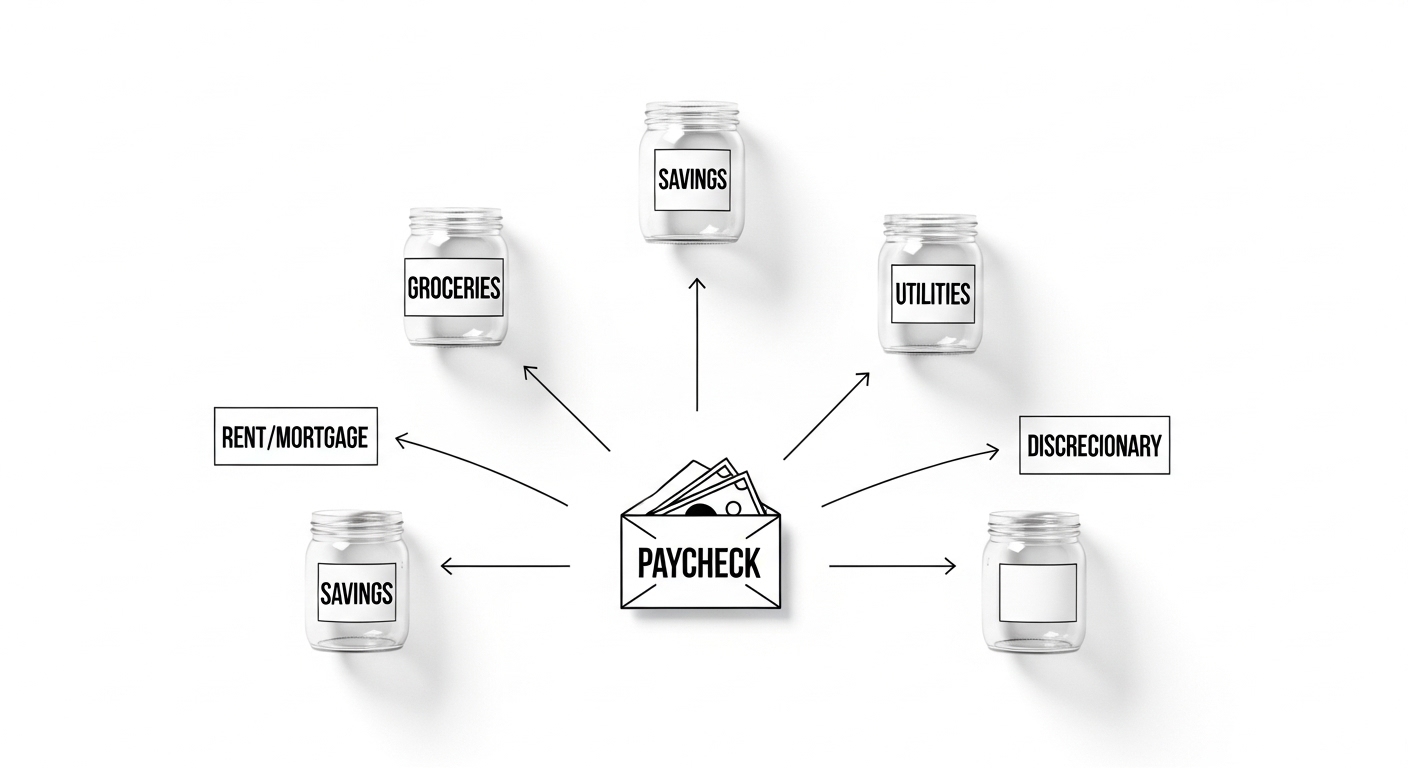

#3 — Rename Your Savings Accounts

Most banks let you label savings accounts with custom names. Calling a savings pot 'Emergency Fund' feels abstract and vaguely punishing. Calling it 'Trip to Japan' or 'New Laptop Fund' creates a concrete mental image that makes transfers feel rewarding rather than restrictive. Behavioral economists sometimes call this 'mental accounting' — and while it can work against you in some contexts, here it works squarely in your favor.

Renaming a savings account from 'Savings' to a specific goal can meaningfully increase how often people contribute to it — the label changes the emotional relationship with the money.

#4–#6: Structural Tricks That Run on Autopilot

#4 — Automate a 'Round-Up' Transfer

Several banks and apps now offer automatic round-up features: every purchase gets rounded to the nearest dollar, and the difference goes into savings. Spend $4.60 on coffee, and $0.40 moves to savings. It sounds trivial, but figures vary — estimates suggest active users can accumulate a few hundred dollars annually without noticing. The power is not the amount; it's the complete removal of willpower from the equation.

If your bank doesn't offer this natively, you can replicate it manually with a weekly transfer of whatever small amount feels invisible. The key word is 'invisible.'

#5 — The Subscription Audit (Do It Quarterly, Not Once)

Most people do a subscription audit once, feel virtuous, and then quietly accumulate new ones over the following year. The gym app from January. The news site from an election cycle. The streaming service a friend recommended and never mentioned again. Doing this quarterly — not annually — catches the drift before it compounds.

A practical method: pull up your last two months of bank statements and highlight every recurring charge. Then ask whether you'd sign up for each one today, at today's price, knowing what you know now. The answer is often no.

#6 — Pay Yourself First, But Make It Awkward to Undo

Automatic savings transfers set to hit the day after payday are standard advice. The less-discussed upgrade is making the savings account slightly inconvenient to access — a different bank, no debit card attached, a two-day transfer delay. Friction is a feature, not a bug. The small annoyance of accessing the money is often enough to prevent casual withdrawals that erode the balance.

#7–#9: Unconventional Tactics Most Lists Skip

#7 — Negotiate Bills You've Never Thought to Negotiate

Internet service, insurance premiums, and even medical bills are frequently negotiable — and most people never try. Telecom companies in particular have retention departments whose entire job is to offer discounts to customers who call and say they're considering leaving. A single 15-minute call can cut a monthly bill by a meaningful amount, and that saving repeats every month without further effort.

The counterintuitive part: loyalty is often penalized, not rewarded. Long-term customers frequently pay more than new customers for identical services. Calling to renegotiate essentially resets you to 'new customer' pricing.

Loyalty to a service provider is often financially punished — long-term customers routinely pay higher rates than new sign-ups for the exact same plan.

#8 — Use 'No-Spend Days' as a Diagnostic Tool, Not a Punishment

A no-spend day — where you commit to zero discretionary purchases for 24 hours — is usually framed as a savings tactic. It's more useful as a diagnostic. Most people who try it discover exactly which spending habits are automatic versus intentional. The coffee on the way to work, the lunchtime browse, the evening app purchase — these only become visible when you try to stop them.

Once you know which habits are running on autopilot, you can decide which ones are actually worth the money. Some will be. Many won't.

#9 — Buy Experiences in Advance, Not Things

Pre-purchasing experiences — a cooking class, a concert, a weekend trip — tends to generate more lasting satisfaction than buying objects, according to a fairly consistent body of research in psychology. But there's a savings angle here too: buying experiences during off-peak or early-bird windows is almost always cheaper than buying on impulse close to the date. You save money and get something that research suggests makes you happier. That's a rare double win.

#10 + Bonus Pick: The Habits That Compound Over Years

#10 — The 'One In, One Out' Rule for Possessions

Every time something new enters your home, something old leaves — sold, donated, or discarded. This rule is usually discussed as a decluttering strategy, but the financial effect is real. Selling the outgoing item offsets part of the new purchase cost. More importantly, the rule creates a natural pause before buying anything, because you have to mentally identify what you'd remove to make room for it. That pause kills a surprising number of purchases before they happen.

Anyone who has moved house and confronted the sheer volume of things they own but never use understands why this rule has teeth.

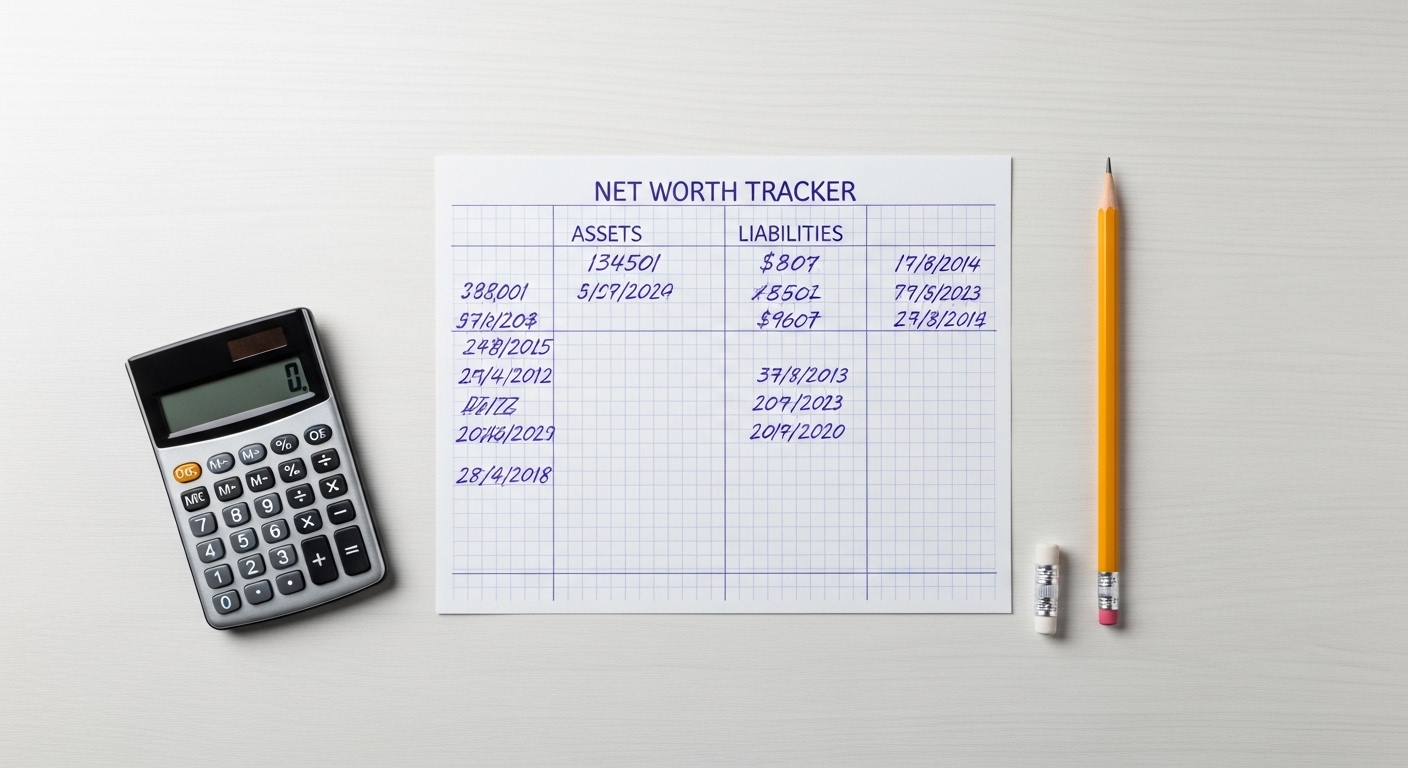

Bonus Pick — Track Net Worth Monthly, Not Just Spending

Budgeting apps focus on cash flow — money in, money out. But tracking net worth (assets minus liabilities) once a month gives you a completely different signal. A month where you spent more than usual but paid down debt or saw investments grow can still be a 'good' financial month. Conversely, a month where spending looked fine but a car lost significant value is a net-worth loss. The number that actually matters is the one most people never look at.

(Opinion: The savings advice industry has a vested interest in making this feel complicated. Most of what actually works is boring, structural, and requires about 30 minutes to set up. The elaborate systems and apps are largely for people who enjoy the hobby of personal finance — which is fine, but not necessary.)

Frequently Asked Questions

Do these saving methods work if you're already on a tight budget?

Several of them work especially well on tight budgets. Negotiating bills, doing subscription audits, and using the cost-per-use reframe don't require you to have extra money — they reduce what's going out. The round-up and automation tactics work best once there's a small buffer, but even a $5 automatic weekly transfer builds the habit before the amount scales up.

Is it really worth calling to negotiate a bill like internet or insurance?

For most people, yes. Retention departments at telecom and insurance companies have real authority to offer discounts, and the worst outcome is being told no. The call typically takes under 20 minutes. Estimates vary, but many people report saving anywhere from $10 to $50 per month on a single bill — which adds up to a meaningful annual figure over time.

Why do labeled savings accounts actually help — isn't it just psychological?

It is psychological, and that's exactly why it works. The brain doesn't treat money as a perfectly fungible resource — it assigns different emotional weights to different 'pots,' even when the underlying dollars are identical. Using that tendency deliberately, rather than fighting it, is one of the more practical insights from behavioral economics. 'Just psychology' undersells how much of financial behavior is driven by framing rather than logic.

The most unsettling thing about this list isn't any single tactic — it's what the list implies collectively. Most of the money that quietly disappears from people's finances doesn't go to big, memorable purchases. It goes to friction-free, forgettable ones: the subscription that auto-renewed, the bill nobody questioned, the item bought on impulse and used twice. The piggy bank was never the problem. The invisible leaks were.

Comments

Post a Comment